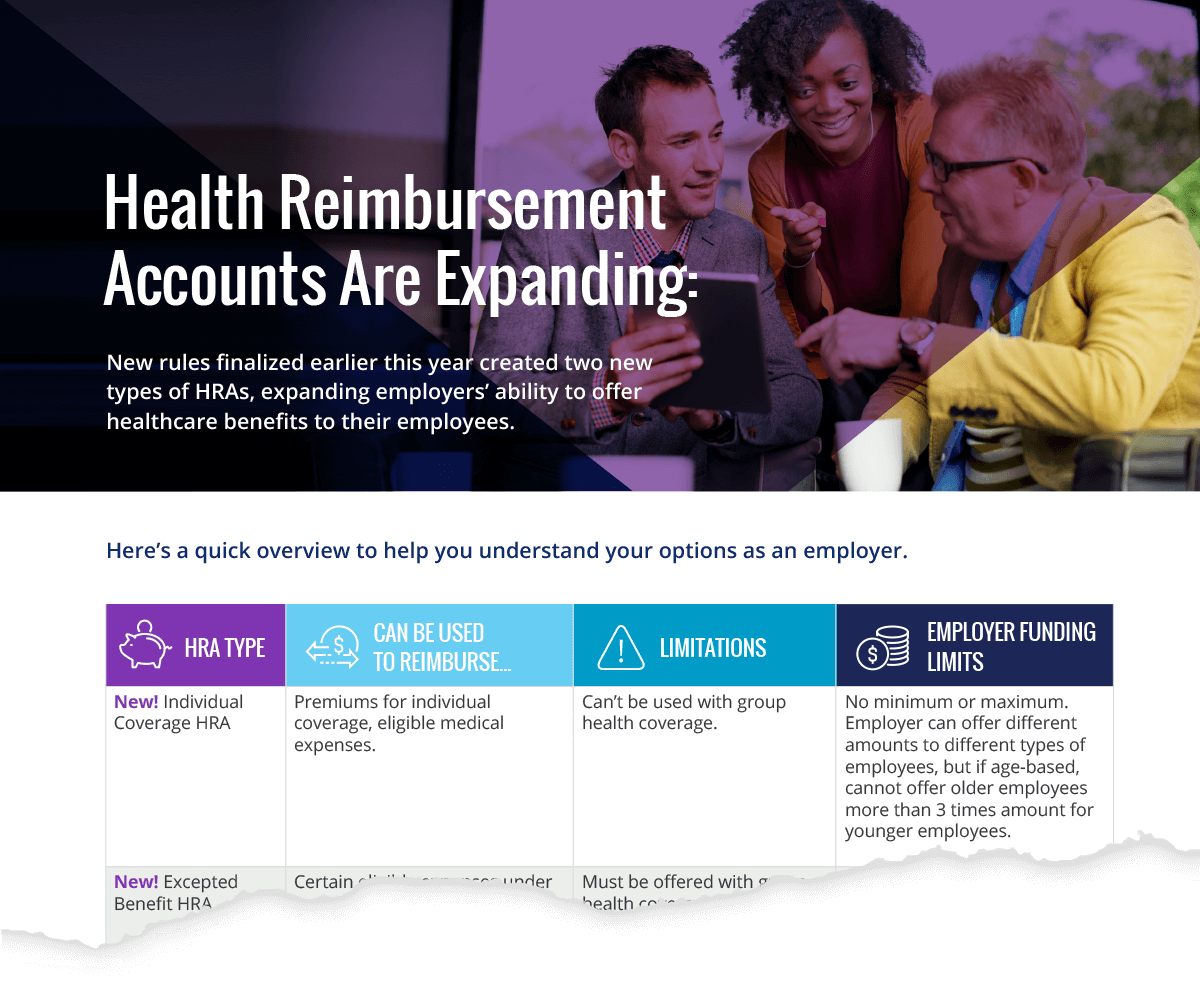

Will Individual Coverage HRAs Usher in Defined Contribution for Healthcare Benefits…and Should They?

When 401k defined contribution (DC) plans were introduced in the late ‘70s, they were considered ground-breaking—a word also being used to describe ICHRAs.

Some are already predicting that ICHRAs will change the benefits landscape as employers seek to stabilize their healthcare cost liabilities by replacing group coverage with these accounts, while promoting a new level of employee consumerism. They may be right. We don’t have a crystal ball and can’t predict the future.

But, we can’t help wondering if there are some parallels with 401k plans and perhaps a cautionary tale for employers to consider before rushing to replace group health coverage with ICHRAs.

Way back when, 401k plans were fringe.

401k plans enabled individual employees to put away their own money on a tax-advantaged basis to augment their employer’s pension plan or other retirement benefits. Sure, the employee bore all the risk and had to make all the investment decisions, but that was okay because their DC plan at that point was essentially gravy. No one was relying on it for their retirement security. It was considered the third leg of the “three-legged stool” of retirement—pension, Social Security and 401k.

DC plans enabled employers to offer the opportunity for additional retirement saving at a nominal cost. They had no requirement to provide a contribution or match to employees, although many did. The three-legged stool was alive and well.

Over time, however, the DC approach to retirement won out from a cost perspective, precisely because the employee effectively funded it and took on the responsibility for their own retirement. Instead of carrying the liability of funding a defined benefit retirement approach, employers could (and did) defund or terminate their pension plans. Many now sponsor and contribute exclusively to employees’ 401k plans.

Pensions are no more.

Today, just 13% of private sector employees have a pension. And, pensions aren’t generating much income. The median pension payout was just $9,262 in 2016. Still, most employees are facing retirement without the prospect of even a modest amount of guaranteed income from an employer pension plan.

Even though DC plans are popular, a full 35% of employees don’t have access to save for retirement through an employer-sponsored 401k. Of those with access to a plan, less than 75% participate. And, of those who do participate, 42% have less than $10k saved although the number increases with age.

This shift in funding responsibility from employer to employee, combined with employees’ lack of financial expertise, are two contributing factors to the anticipated retirement crisis.

Lack of retirement savings is causing financial strain and stress.

From an employer’s perspective, employees’ lack of retirement security and overall poor financial well-being is a serious issue. According to PwC’s 2018 Employee Financial Wellness Survey, financial stress impacts people’s work engagement and productivity. It makes them more likely to call in sick, or even seek employment with an organization they feel is more supportive of their financial well-being.

Employees are using the 401k to cover medical costs.

And, there’s a healthcare connection to heed. The PwC survey found that employees’ number-one response to what would help them achieve their future financial goals was lower healthcare costs. Almost a quarter of employees indicated they would be willing to forgo future pay increases for better healthcare benefits.

Employees are also eyeing their retirement savings for medical bills. Forty-two percent felt they were likely to have to dip into a retirement account in the future and, of these, 25% believed it would be because of a healthcare cost.

Was the rise of the 401K bad? Not necessarily, but ICHRAs could have a similar effect.

In hindsight, it’s easy to see how the move to DC retirement plans has contributed to a lack of financial well-being for many working Americans, but it’s certainly not the only factor or even a primary one. The demise of the pension and the rise of the 401k may simply represent the natural evolution of benefits, which are tied to the economic well-being and productivity of employers and reflect emerging social and demographic realities. Benefits help recruit, retain and reward employees, and the needs of both employers and employees change over time—so benefits change too.

And, we’re not looking to rain doom and gloom over ICHRAs, because they do offer a unique opportunity for employers to leverage them as a solution for populations with unmet benefits needs.

Indeed, ICHRAs are perfect for extending benefits to employees who were previously ineligible, particularly part-time workers. This is vital given today’s labor market, where competition is tight for all types of employees, and companies like Starbucks and others are focusing on recruiting and retaining part-time employees with richer benefits.

ICHRAs are an ideal solution for this population. They enable an employer to subsidize all or part of the employee’s healthcare coverage without extending group health coverage.

If this is indeed a cautionary tale, it’s certainly one with a happy and flexible ending. While ICHRAs may ultimately usher in an era of defined contribution for employee healthcare, in this economic environment and tight labor market, ICHRAs might be best seen as a mechanism to extend coverage to a previously uncovered group of employees with little or no risk and stable cost to the employers. ICHRAs may be just the answer many employers are looking for to strengthen their recruitment and retention strategies around this vital portion of their workforce.